Bengal’s Geoeconomic Moment: Can BJP’s Victory Reposition India’s Eastern Trade Gateway?

- Dhriti Mukherjee Pipil

- May 8

- 7 min read

History gave Bengal geography. Geopolitics may now be giving it another chance.

For decades, West Bengal represented one of the great unrealised geoeconomic opportunities of South Asia. Few Indian states possess a comparable strategic location. Bengal sits at the intersection of the Bay of Bengal maritime system, Bangladesh’s manufacturing economy, the Northeast, the Himalayan transit corridor, and India’s Act East framework. Kolkata was once among Asia’s leading commercial cities, connecting riverine trade, shipping, finance, and manufacturing across the eastern subcontinent.

Yet geography alone does not create economic power. Ports without cargo ecosystems become transit points. Borders without logistics integration become bottlenecks. Strategic location matters only when institutions convert connectivity into production, trade, and investment.

That conversion largely failed in Bengal during India’s post-1991 globalisation phase.

While western India integrated rapidly into containerised trade, export manufacturing, industrial corridors, and global capital flows, eastern India remained comparatively under-integrated within modern logistics and supply-chain systems. The result was not merely Bengal’s relative decline. India itself developed an imbalanced trade geography in which western ports, industrial belts, and freight corridors absorbed disproportionate economic momentum.

The BJP’s decisive victory in West Bengal, therefore, raises a larger question extending far beyond state politics: can India finally reposition Bengal as the anchor of an eastern trade and logistics corridor at a time when global supply chains themselves are being reorganised?

This question matters because the world economy is entering a fundamentally different phase of globalisation.

The End of Hyper-Globalisation

The earlier era of hyper-globalisation was driven primarily by efficiency. Firms concentrated manufacturing where costs were lowest, supply chains became deeply integrated across borders, and maritime trade expanded through highly optimised production networks.

That model is now under strain.

The COVID-19 pandemic, the Russia–Ukraine conflict, Red Sea disruptions, sanctions regimes, and intensifying U.S.–China rivalry exposed the vulnerabilities of concentrated supply chains and excessive dependence on a limited set of manufacturing geographies and shipping routes.

Governments increasingly prioritise resilience, strategic autonomy, trusted production networks, and logistics diversification alongside efficiency. As a result, trade corridors are no longer merely infrastructure projects. They are becoming instruments of geopolitical influence.

China’s Belt and Road Initiative, the India–Middle East–Europe Economic Corridor, the International North–South Transport Corridor, and Indo-Pacific connectivity initiatives all reflect a broader global contest over ports, freight systems, industrial ecosystems, and maritime routes.

In this changing environment, eastern India is regaining strategic relevance.

The Bay of Bengal is steadily re-emerging as one of the Indo-Pacific’s most important commercial theatres. Simultaneously, Bangladesh has evolved into one of Asia’s fastest-growing manufacturing economies, multinational firms are pursuing China+1 diversification strategies, and India’s Act East Policy is pushing economic attention toward eastern connectivity systems.

The next phase of globalisation may reward logistics gateways and transit economies as much as low-cost manufacturing centres.

That creates a potentially historic opening for Bengal.

Bengal Missed India’s First Globalisation Cycle

Bengal’s challenge was never geography. It was institutional execution.

Post-liberalisation India witnessed the rapid rise of western and southern industrial corridors integrated with modern ports, freight systems, and export-oriented manufacturing ecosystems. Gujarat, Maharashtra, Tamil Nadu, Andhra Pradesh, and Karnataka increasingly positioned themselves within global production networks through aggressive infrastructure expansion, industrial clustering, logistics modernisation, and investor-oriented governance.

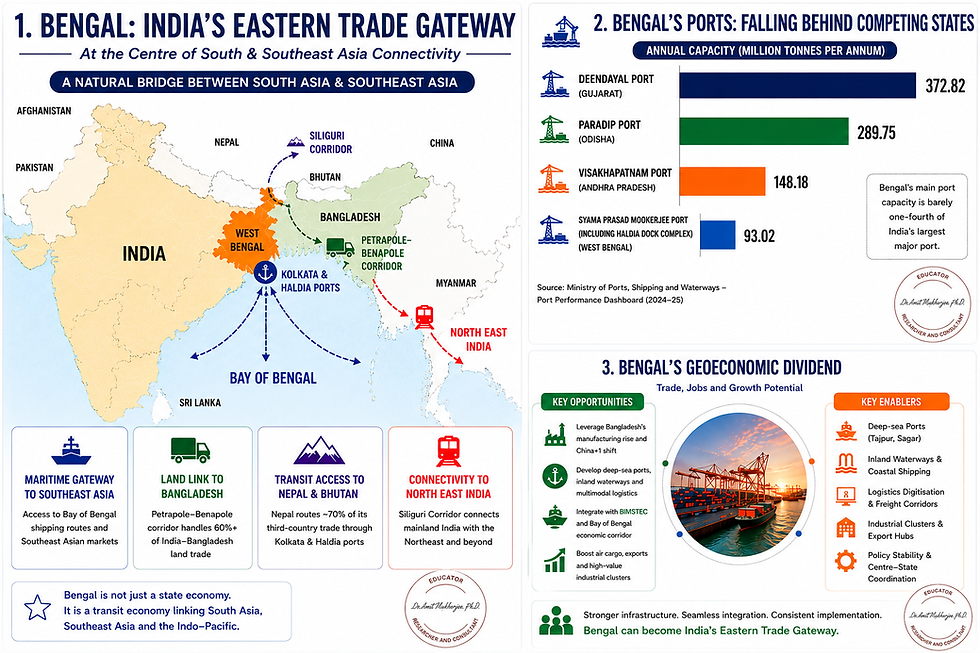

Eastern India lagged. The divergence became especially visible in maritime infrastructure. Ports such as Mundra, Deendayal, Jawaharlal Nehru Port, Paradip, Chennai, and Visakhapatnam expanded alongside industrial corridors and integrated logistics systems. Bengal’s maritime infrastructure modernised far more slowly.

The consequences are now measurable.

Syama Prasad Mookerjee Port, including Haldia Dock Complex, operated at roughly 93 million tonnes per annum capacity during 2024–25. By comparison, Visakhapatnam crossed 148 million tonnes, Paradip nearly 290 million tonnes, and Deendayal Port exceeded 370 million tonnes annually.

This divergence reflects more than cargo statistics. It reflects the redistribution of India’s trade geography.

The same pattern appeared in investment flows. More than 6,600 companies reportedly shifted their registered offices out of Bengal between 2011 and 2026. FDI inflows remained modest relative to major industrial states, while rising debt increasingly constrained fiscal flexibility.

The deeper issue was not merely slower growth.

Bengal gradually lost integration with the country’s evolving export economy precisely when Asian manufacturing geography was being rewritten.

The Bay of Bengal Manufacturing Arc

No external economic relationship is more strategically important to Bengal today than Bangladesh.

Over the past two decades, Bangladesh has emerged as the world’s second-largest ready-made garment exporter and one of Asia’s fastest-growing manufacturing economies. As multinational firms diversify production beyond China, the Bay of Bengal region is gradually evolving into an important secondary manufacturing and logistics space within the Indo-Pacific.

Bengal was structurally positioned to become central to this transformation.

The state shares a 2,217-kilometre border with Bangladesh alongside deep linguistic, cultural, and commercial linkages. The Petrapole–Benapole corridor already handles the majority of India–Bangladesh land trade, making it one of South Asia’s most strategically important border gateways.

Yet for years, inadequate warehousing, customs delays, congestion, fragmented multimodal connectivity, and weak logistics integration constrained the corridor’s larger economic potential.

That missed opportunity matters because modern manufacturing increasingly depends upon regional production ecosystems rather than isolated national industries.

A more integrated eastern corridor could support cross-border value chains in engineering goods, pharmaceuticals, food processing, fisheries, textiles, packaging, leather, logistics services, and light manufacturing. Border infrastructure is no longer merely about trade facilitation. It increasingly determines whether regions integrate into wider production networks.

The same logic extends to BIMSTEC.

The BIMSTEC grouping, comprising Bangladesh, Bhutan, India, Myanmar, Nepal, Sri Lanka, and Thailand, represents nearly 1.7 billion people and a combined GDP exceeding $5 trillion. Yet intra-regional trade remains disproportionately low compared with ASEAN.

That gap between economic potential and actual integration represents one of Asia’s largest unrealised commercial opportunities.

Bengal occupies the geographic centre of this emerging Bay of Bengal architecture. If integrated effectively through ports, coastal shipping, rail corridors, inland waterways, logistics parks, and border industrial ecosystems, Bengal could emerge not merely as a state economy but as India’s principal eastern commercial interface with South and Southeast Asia.

Geoeconomics: Bengal’s Logistics Deficit in the China+1 Era

However, strategic location alone no longer guarantees commercial centrality.

Modern trade increasingly depends upon logistics efficiency, cargo velocity, multimodal integration, draught depth, warehousing ecosystems, digital customs systems, and freight reliability.

This is where Bengal’s structural weaknesses remain most visible. The state continues to face a major maritime deficit. Kolkata and Haldia remain strategically important to eastern India’s trade system, but both face significant draught limitations. Larger vessels frequently require cargo lightening or rerouting toward deeper ports elsewhere. In an era where shipping economics increasingly reward scale and turnaround efficiency, shallow-draught infrastructure directly affects competitiveness. The prolonged indecision surrounding the Tajpur and Sagar deep-sea port projects further weakened Bengal’s maritime position. Despite possessing one of India’s most strategically valuable coastlines, Bengal still lacks a modern deep-sea port integrated with large-scale logistics and industrial ecosystems.

The inland waterways deficit compounds the problem.

Historically, Bengal formed part of one of Asia’s great riverine commercial systems through the Ganga–Brahmaputra network. National Waterway-1, stretching from Haldia to Prayagraj, passes through a region generating enormous freight potential. Yet inland water transport remains severely underutilised despite offering lower logistics costs and multimodal advantages.

The same pattern appears in air cargo. Kolkata airport achieved record cargo throughput in 2024–25, yet high-value export products from eastern India, including seafood, floriculture, Darjeeling tea, leather goods, and processed foods, continue to depend significantly upon western and northern cargo hubs.

This raises transaction costs, delays exports, and weakens competitiveness.

The problem is not a lack of economic potential.

The problem is the failure to integrate Bengal into modern supply-chain architecture during a period when logistics itself became a strategic industry.

The Siliguri Corridor and Eastern Freight Geography

North Bengal may become equally important in the coming decade.

The Siliguri Corridor, often viewed narrowly through a security lens, also represents one of South Asia’s most consequential freight corridors. This narrow stretch connects mainland India with the Northeast while simultaneously linking India with Nepal, Bhutan, Bangladesh, and the eastern Himalayan region.

Nearly all surface freight moving toward the Northeast passes through this geography.

Nepal and Bhutan remain heavily dependent upon Indian transit systems and Bengal’s port infrastructure for third-country trade. As regional connectivity expands, North Bengal possesses significant potential for warehousing ecosystems, dry ports, cargo consolidation centres, freight terminals, and multimodal logistics integration.

In corridor-driven economies, transit geography itself becomes an economic asset.

The countries and regions controlling logistics nodes increasingly influence trade flows, manufacturing location decisions, and supply-chain architecture.

This is precisely why connectivity is becoming a form of geopolitical power.

From Welfare Politics to Export-Led Growth?

The deeper economic question confronting Bengal extends beyond infrastructure.

Can the state transition from a consumption-driven political economy toward a production- and export-oriented growth model?

Long-term employment generation ultimately depends upon productive investment, industrial ecosystems, tradable sectors, and logistics-linked economic activity. Welfare expansion can stabilise consumption and reduce distress, but sustained structural transformation historically emerges from production growth, export competitiveness, and private-sector job creation.

This is particularly relevant for Bengal’s labour market.

For years, the state witnessed sustained migration of skilled workers toward Bengaluru, Hyderabad, Pune, Delhi, and Mumbai because Bengal struggled to generate comparable industrial and services-sector employment ecosystems.

A serious export-oriented development strategy could partially alter that trajectory.

Ports, logistics systems, industrial corridors, border trade infrastructure, and freight ecosystems generate layered employment across warehousing, transport, customs services, cold-chain logistics, engineering, food processing, maritime services, packaging, digital trade systems, and manufacturing.

Several central initiatives already provide the policy framework for such transformation: PM Gati Shakti, Sagarmala, Bharatmala, inland waterways development, Production Linked Incentive schemes, and the Districts as Export Hubs initiative.

What Bengal historically lacked was coordinated execution.

Trade corridors require synchronisation across customs systems, ports, highways, railways, industrial policy, external trade strategy, warehousing, and logistics regulation. Fragmented governance raises transaction costs and weakens competitiveness.

Political alignment between the Centre and the state potentially reduces one longstanding institutional friction.

But alignment alone does not modernise a port, clear a freight bottleneck, or attract manufacturing capital.

Execution will determine whether this political transition produces structural economic change or merely another cycle of unrealised expectations.

Conclusion: Bengal’s Strategic Window

So, can Bengal finally reposition itself within India’s evolving trade geography?

The structural conditions are arguably more favourable today than at any point since liberalisation.

Global supply chains are fragmenting. China+1 diversification is reshaping manufacturing decisions.

Corridor competition is intensifying. The Bay of Bengal is regaining strategic importance. India’s eastern connectivity systems are becoming increasingly relevant within the Indo-Pacific economy.

At the same time, political alignment between the Centre and the state reduces one of Bengal’s longest-standing institutional constraints.

But history also offers a warning.

Strategic geography creates opportunities. It does not guarantee outcomes.

The regions that dominate twenty-first-century trade may not necessarily be those with the largest populations or cheapest labour. Increasingly, they may be the regions that control logistics systems, multimodal corridors, maritime connectivity, and supply-chain reliability.

Connectivity itself is becoming a strategic power.

The central question, therefore, is whether Bengal can finally convert its geography into economic leverage through ports, freight systems, industrial ecosystems, and regional trade integration.

If executed effectively, Bengal could emerge as India’s principal eastern trade gateway and a major logistics interface connecting South Asia, Southeast Asia, and the wider Indo-Pacific.

If not, the next phase of Asian trade integration may consolidate elsewhere while Bengal once again watches a historic geoeconomic opportunity pass by.

Comments